Steve's Update (9/8/23) Understanding Our Federal Budget

Steve's Update (9/8/23) Understanding Our Federal Budget

Please Share and Subscribe!

This week I compiled a post I published about a year ago that I think many people would benefit from. I took the US budget and I tried to simplify it. Hopefully it proves interesting and useful to you. Let me know what you think!

Understanding Our Federal Budget:

Our federal budget is huge, roughly $5.8 trillion dollars. When I say our budget, I mean it, it’s ours. Yours and mine.

There are an overwhelming number of programs that make up that $5.8 trillion in spending. Do you need to be a PhD economist to understand the budget? No!

I’m going to try and explain the federal government spending and revenue in an easy-to-understand format. I will use the CBO’s estimates for 2022 for my numbers. When I say something like, Medicare costs us $941 billion, what I mean is the CBO is projecting Medicare to cost $941 billion in 2022. This projection came out in May of 2022, it should prove fairly accurate for the remainder of the year. Things do change, but despite what the news headlines would imply, the big picture in Americas finances hasn’t changed in many years, so while my numbers won’t be spot on accurate, for our conversation the numbers work well.

Let’s get started!

In 2022 the CBO is projecting:

Revenue: $4,836,000,000,000 ($4.8 Trillion)

Spending: $5,872,000,000,000 ($5.8 Trillion)

$4,836,000,000,000 - $5,872,000,000,000 = -$1,036,000,000,000

Deficit: $1,036,000,000,000 ($1 Trillion)

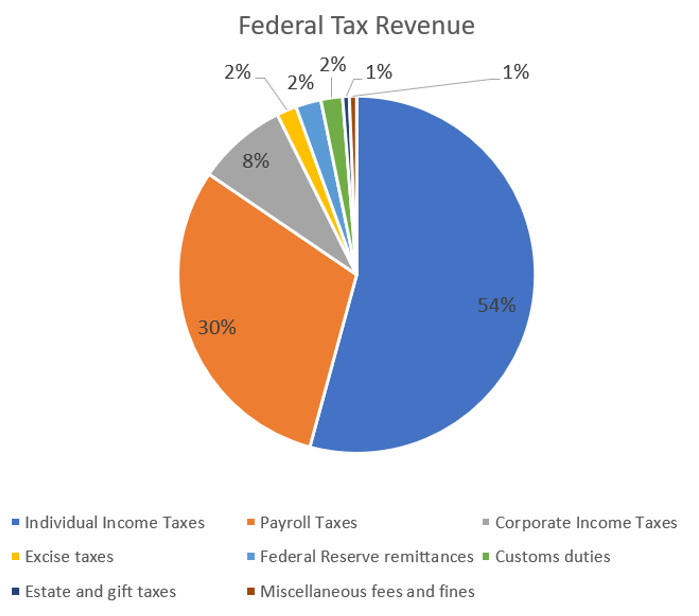

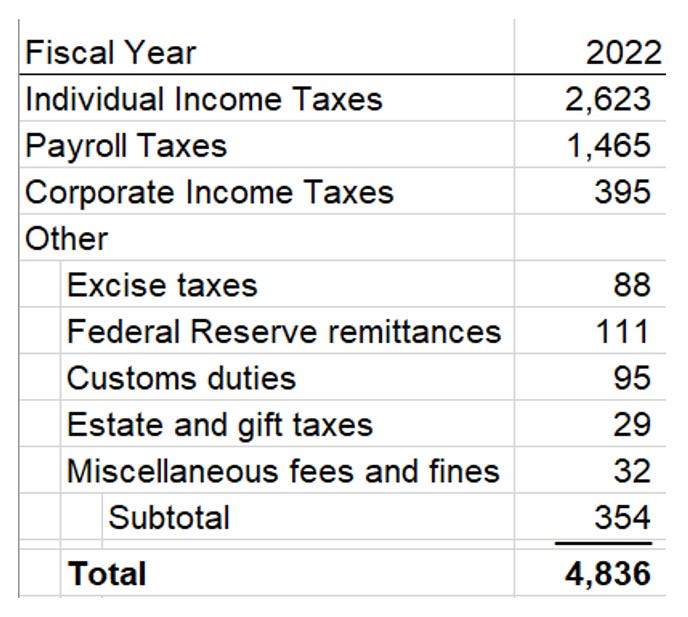

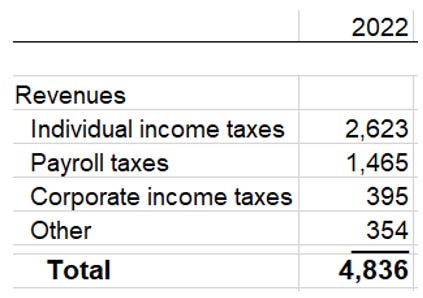

Fiscal revenues:

There will be roughly $4.836 trillion of revenue in 2022. It’s hard to predict this because most taxes are not flat but based on a percentage of income. Of that $4.836 trillion: (Don’t let this intimidate you! Keep reading!)

If you’re running for office, give me a call and we can dive into the details. If you’re just looking to be an informed citizen, think of the revenues coming from 4 areas:

84% of all federal revenue comes from individual income taxes, and payroll taxes. When you hear politicians talk about raising taxes to offset spending, these are the only two areas you need to pay attention to in terms of worrying about our nations fiscal position. What are they doing with the payroll tax, and income taxes. Those are the needle moving taxes. Do corporate income taxes matter? Of course! But if the discussion is on slight adjustments in rates, then the only taxes that really matter are income and payroll taxes.

Individual income taxes

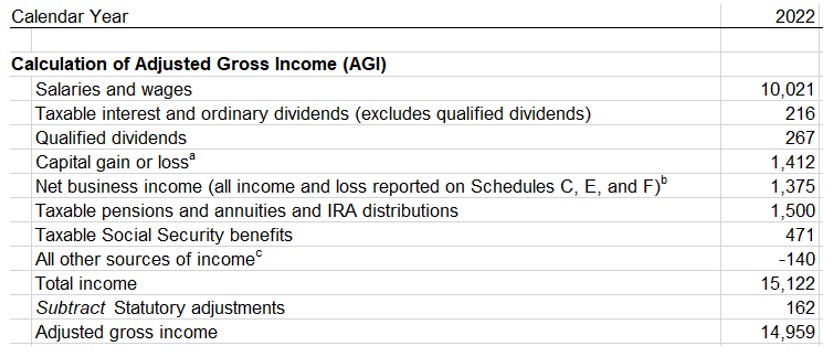

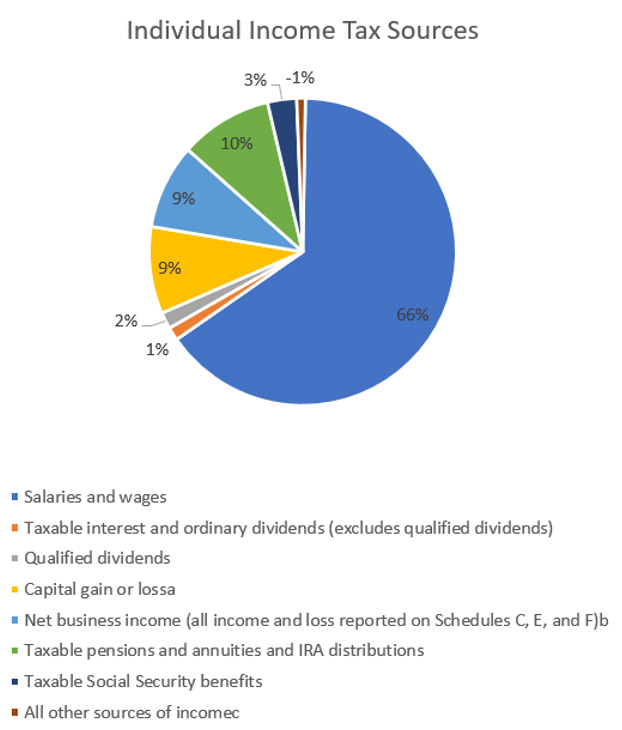

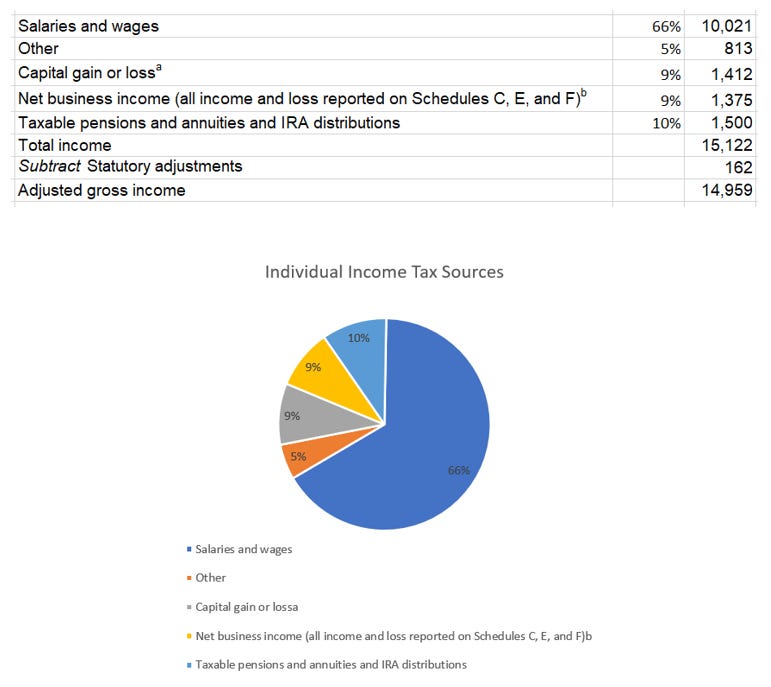

This part gets somewhat complicated, but it is important you wrap your head around it. First, the scary overwhelming charts:

Just understanding salaries and wages gets you 2/3rds of the way there. But to take it a step further, if you can wrap you head around 4 sections, you understand 95% of individual income tax sources.

Salaries and wages are the taxes you are likely most familiar with, if you are a W2 wage earner, these are your taxes that you file and pay every year. Congrats, you’re the most important source of revenue to the US government, hurray you!

In this chart, you are looking at the total amount of reported salaries. We had $10 trillion of reported wages in the US. This does not mean there was $10 trillion in taxes, this is the total amount of wages, that they then tax a certain percentage of.

Net business income is, basically, income earned from small business owners and contractors. The contractor that redid your kitchen, the local pizza shop, they are all likely in this category. They are treated very similarly to you, with two key differences. The first key difference is they have a whole range of deductible expenses that they can use to write off income. The second difference is they self-report their income. When you work a W2 job, your employer reports to the IRS what they paid you. There is nothing in it for your employer to lie, and if they did lie, they could get in huge trouble. And of course, by trouble I mean having to pay a huge penalty tax! Self-employed individuals report their own incomes. Most don’t lie, however, from time to time, some might prove forgetful of a few payments here and there and maybe they add a few expenses that probably happened. An argument for funding the IRS more, is that an increased IRS budget will limit people’s ability to creatively report income. Top of Form

Lastly for income tax, Taxable pensions, annuities, and IRAs make up a big chunk of income tax revenues. Essentially once you are in retirement, money you get from certain pensions, annuities and traditional retirement accounts, get taxed as ordinary income. Annuities can get complicated, because some capital gains get mixed in there, but I would really focus on IRAs; these include: traditional 401(k)s, IRA’s, 403(b)s, individual k’s, and a few other retirement accounts. I’m talking about traditional retirement accounts, not ROTH accounts which are non-taxable in retirement. In retirement when you take a withdrawal from your IRA, whether voluntarily or in the form of a required distribution, that money counts as ordinary income, which means it is treated just like your W2 wages and you pay the same rate minus the payroll tax. Which brings us to the payroll tax!

The payroll tax is a really interesting tax. It’s basically a hybrid individual income tax and corporate tax. In a way, this is a really great place to tax corporations, if they want American workers, they have to pay this tax. You can’t fill out paperwork and claim to be an Irish company to get out of this one. On the flip side, you really could argue it’s money directly out of your potential paycheck. Those small business owners I just accused of creatively reporting income, (sorry gang) they have to pay both sides of this tax for their personal income, the corporate and personal tax.

Federal Spending- You’re saying $4.8 trillion isn’t enough?

In 2022 we’re projected to spend $5.8 trillion. Let’s break it down.

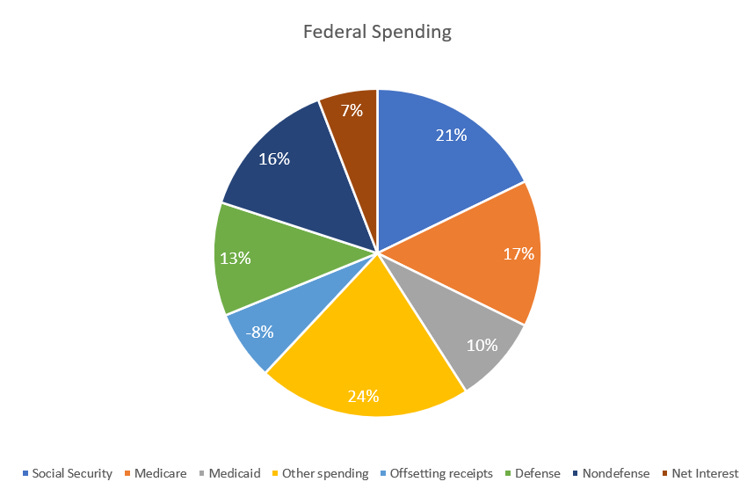

First, the big scary chart:

Immediately you can see the spending side is a bit more divided up. Rest assured; we can still make this digestible. Before we chop it up, I want to talk about Mandatory vs Discretionary spending.

You will hear people talk a lot about mandatory and discretionary spending. Unless you’re personally navigating the halls of congress, it is a very unimportant distinction. For you as a citizen, you can largely ignore the difference. It’s all discretionary. Congress can spend what they want and cut what they want.

What is discretionary and mandatory spending?

Mandatory spending means Congress essentially has agreed to pay these expenses until a 60-vote majority in the senate says otherwise. Discretionary spending must get approved by Congress every year. Mandatory just means harder to change politically, discretionary means easier to change.

Alright, let’s simplify this already:

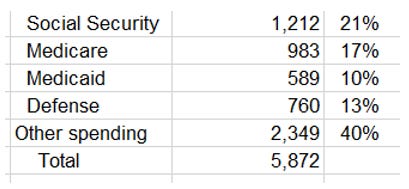

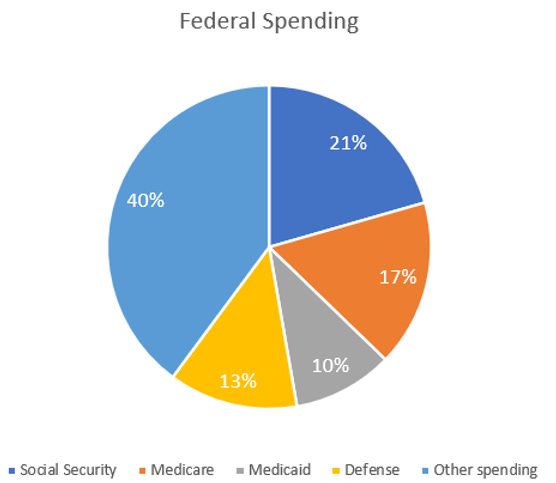

60% of all federal spending comes from 4 categories. Social Security, Medicare, Medicaid, and Defense. I’ll quickly name the four big programs in the “Other spending”: federal civilian and military retirement ($227b), the earned income, child, and other tax credits programs ($220b), SNAP benefits ($159b), and veteran’s programs ($146b). Together they account for about $752 billion.

Now on to the big 4 categories: Social Security ($1.2t), Medicare ($983b), Medicaid ($589b), and Defense ($760b).

Social Security ($1.2t)

Social Security is our social pension system. If you or your spouse worked in the US for 10+ years, you become eligible for a lifetime, inflation adjusted pension starting between age 60-70. As you can imagine, with 10,000 baby boomers turning 65 every day, the federal government sends out a lot of payments to these households.

Medicare ($983b)

Medicare is our nations version of a universal health system only it is explicitly for people over the age of 65. Just like your health insurance at work, people pay a Medicare premium, and when they go to the doctor, Medicare helps pay. Medicare is a huge program and while it is great for the people on it, there’s no denying it is costing our country a lot of money. There’s talk of expanding Medicare to everyone, and that might not be as expensive as it sounds because we currently only cover the most expensive people in the nation to insure, that being the elderly. But unless our nation can manage to stop paying extremely more for health care compared most other highly developed nations, Medicare for all will inevitably cost us a lot of money, just like Medicare for those over 65 does now.

Medicaid ($589b)

Medicaid is our nations version of a universal health system for low-income people. Who counts as low income? Apparently about 20% of Americans do. Nearly all people earning less than 133% of the poverty level are covered under Medicaid. The programs costs are split between the states and the federal government. The $589b is the federal cost. States can partly design the program within their state, and the federal government contributes massively to the cost. General health insurance for low-income people makes up the bulk of the spending, but long-term care expenses for the elderly are very significant too.

To learn more about why we spend egregious amounts of money on health care I can’t recommend this article by Atul Gwande enough: The Cost Conundrum | The New Yorker

Defense ($760b)

Defense is the third largest area of spending. And yet, the first that sounds like a traditional government role. The US spends a lot of money on defense and by any measure we have a very large and well-equipped army. Is it large and well-equipped enough? That’s not really for me to say. $760b makes up around 38% of total defense spending globally, China is #2 on the list with $293b, but I would question the accuracy of that number.

Your feelings on how large our defense budget should be gets into your opinions on what role our armed forces should play in the world and what degree of victory you expect in a whole range of possible confrontations.

Congrats!

If you read this, you are probably now among the absolute top tier educated citizens in regard to our nations fiscal health. It isn’t rocket-science. There is a big picture. The bulk of revenue comes from income taxes and payroll taxes, the bulk of spending goes to Social Security, Medicare/Medicaid, and Defense. In the future I will break down some of these areas more so that you can further understand them.

If you like this post, or think somebody should read it, please share it!

As election season comes you will hear a lot of conversation about spending and taxes. Refer to this post, see if what you’re hearing/thinking fits within the big picture. Often politicians will point to simple fixes or one minor tweak that will totally solve all our fiscal problems. They might stand up on stage and claim that eliminating food stamps ($159b of spending) will fix the problem or double the corporate tax rate ($369b of revenue). Both of those would certainly dent the fiscal problem $1.2T deficit, but neither one solves the problem and the reasons not to do either action have merit too, so those need to be weighed.

Good luck!

See you next week.

My goal is for this to be the ultimate weekly newsletter for Financial Advisors. If you have any ideas for improvement, send me a note!